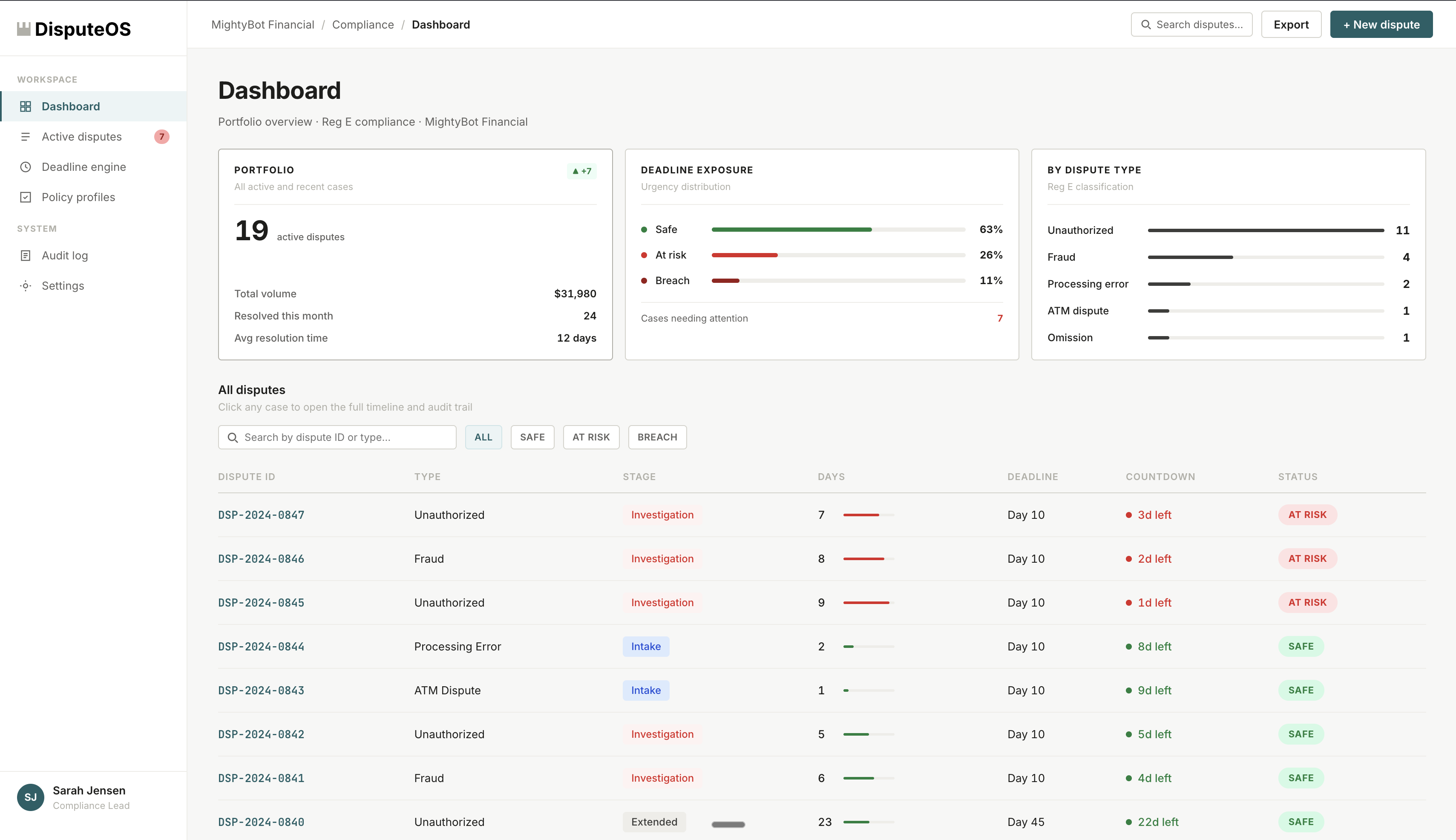

DeadlineShield dashboard: real-time portfolio view with deadline exposure and dispute status tracking

DeadlineShield is the compliance enforcement engine for Reg E, Reg Z, and card network disputes. Deadlines become enforcement gates in your system, not bypassable alerts. When a deadline arrives without the required action, the gate holds. Full audit trail. Examination-ready from Day 0.

What DeadlineShield does: it tracks every open dispute's compliance clock in real time and enforces the required action at each deadline: 10-day investigation, provisional credit, 45/90-day determination. If the action hasn't been taken, DeadlineShield holds the case and escalates to a named human with a full audit record. Your team stays in control. The system makes sure nothing slips.

The CFPB levied $24.7 billion in enforcement actions between 2021 and 2025. The largest Reg E penalty in history landed in January 2025. Every one of these failures started the same way: a system that sent alerts instead of enforcing deadlines.

DeadlineShield is not a single-regulation tool. It enforces compliance clocks across the four regulatory frameworks that govern consumer dispute deadlines at US financial institutions.

Debit card, ATM, ACH, P2P, and prepaid card error resolution under 12 CFR 1005.11.

10 days to investigate or issue provisional credit. 45/90 days for extended determination.

Billing error disputes and credit card chargebacks under 12 CFR 1026.13.

30 days to acknowledge. 90 days (two billing cycles) to resolve.

Visa Claim Resolution and Mastercard chargeback timelines. Network-specific response windows and representment deadlines.

30 days typical response window. Network-specific escalation clocks.

Unauthorized entry return deadlines and ACH dispute resolution timelines under NACHA Operating Rules.

2 business days for unauthorized return. 60 days consumer notification window.

Banks don't fail because they don't know the rules. They fail because their systems treat deadlines as email alerts that can be snoozed, ignored, or routed to someone who is on vacation.

When a consumer reports a dispute, a clock starts. Reg E gives your institution 10 business days to investigate or issue a provisional credit. Reg Z gives 30 days to acknowledge and two billing cycles to resolve. Card networks impose their own response windows. Each dispute can run four or more independent clocks at the same time.

Miss a single clock and you owe the consumer a remedy. Miss a pattern of clocks and the CFPB owns your next three years.

Multi-department routing causes systematic timeline breaches. Holiday calendars get miscounted. Provisional credits get mislabeled. Written confirmations delay investigation starts. An alert says "you should do this by Thursday." An enforcement gate says "you cannot proceed until this is done."

Every penalty in the last three years traces back to the same root cause: the system complained, but didn't enforce.

An alert says "you should do this by Thursday." An enforcement gate says "you cannot proceed until this is done."

Whether you use Fiserv Nautilus, FIS CBK, FINBOA, Quavo, or a spreadsheet, the failure mode is the same. Alerts are not enforcement.

Day 8 email: "Dispute #4721 approaching 10-day deadline." Your analyst is on PTO. The backup analyst has 47 other disputes. The email sits in a shared inbox. Day 11: the deadline passes. Nobody noticed.

Your analyst knows the investigation needs more time. They request the extension. But the provisional credit doesn't post to the consumer's account because the GL integration is a manual step. The system tracks the intent. Reg E requires the action.

Six months later, the CFPB examiner pulls your dispute records and runs a timeline analysis. They find 23% of disputes exceeded the 10-day investigation window without a provisional credit. That is not a one-off mistake. That is a systematic violation.

DeadlineShield replaces the alert model with an enforcement gate model. The system does not notify you that a deadline is approaching. It blocks the dispute from advancing until the required action is completed.

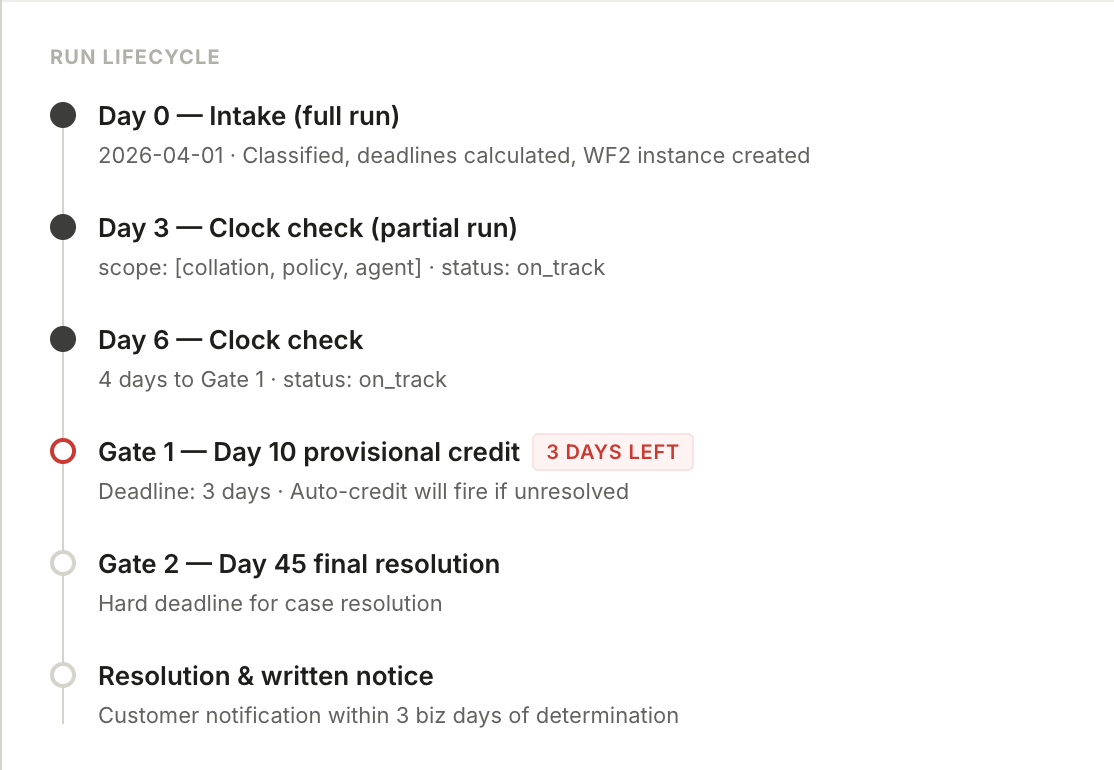

Consumer reports an error (phone, branch, online, mail). The compliance clock starts immediately on oral notice. DeadlineShield determines the clock variant: Reg E standard (10/45), Reg E extended (20/90), Reg Z (30/two billing cycles), or card network timeline. Every subsequent deadline is computed to the business day using your institution's actual holiday calendar.

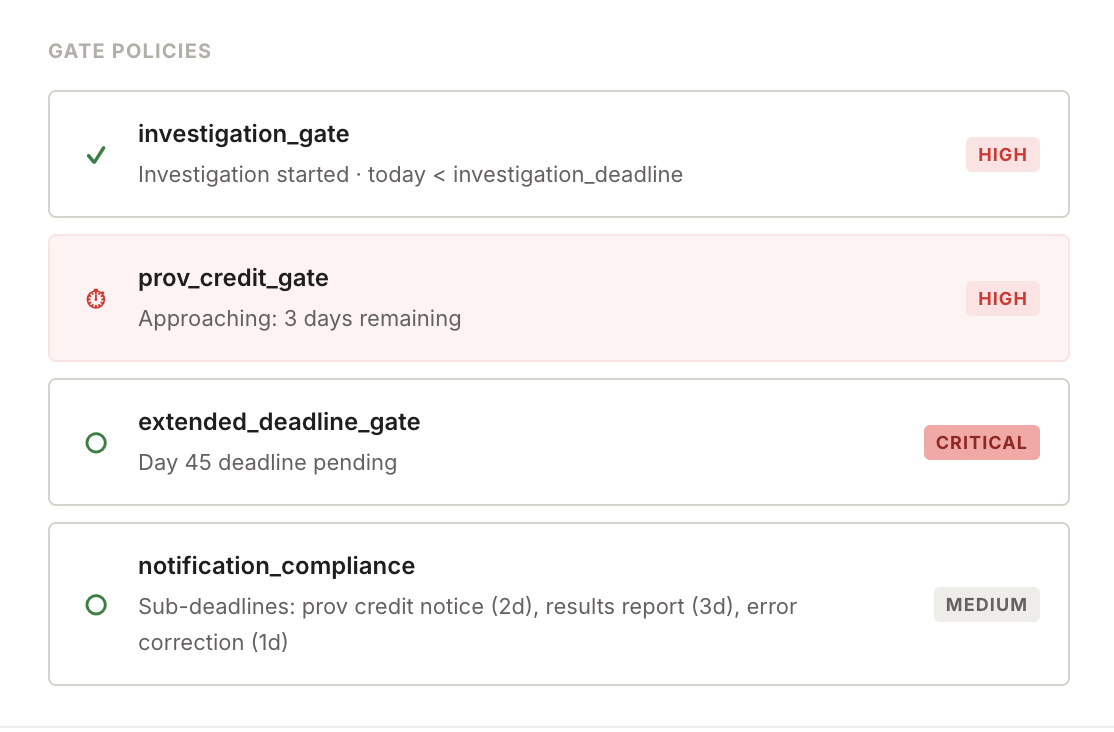

At the deadline mark, the system enforces a gate. Either the investigation is complete and a determination has been made, or the required consumer remedy (provisional credit, acknowledgment letter) must be issued. If neither has happened, DeadlineShield holds the case and escalates to a named human with a full audit trail. No one can advance the dispute without completing the required action.

If the investigation was extended, the next calendar deadline becomes the next gate. The investigation must be completed and the consumer notified within 3 business days. If provisional credit was issued and no error is found, 5 business days notice must be provided before debiting. Every sub-deadline has its own gate.

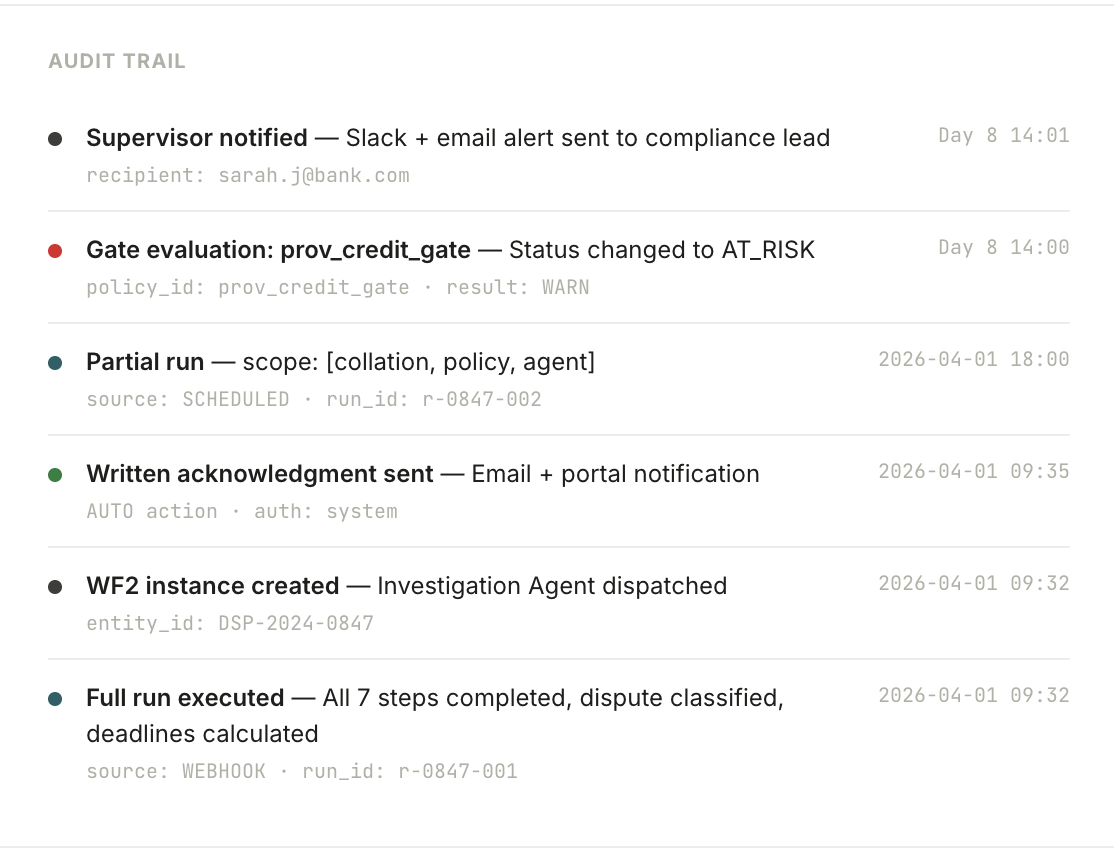

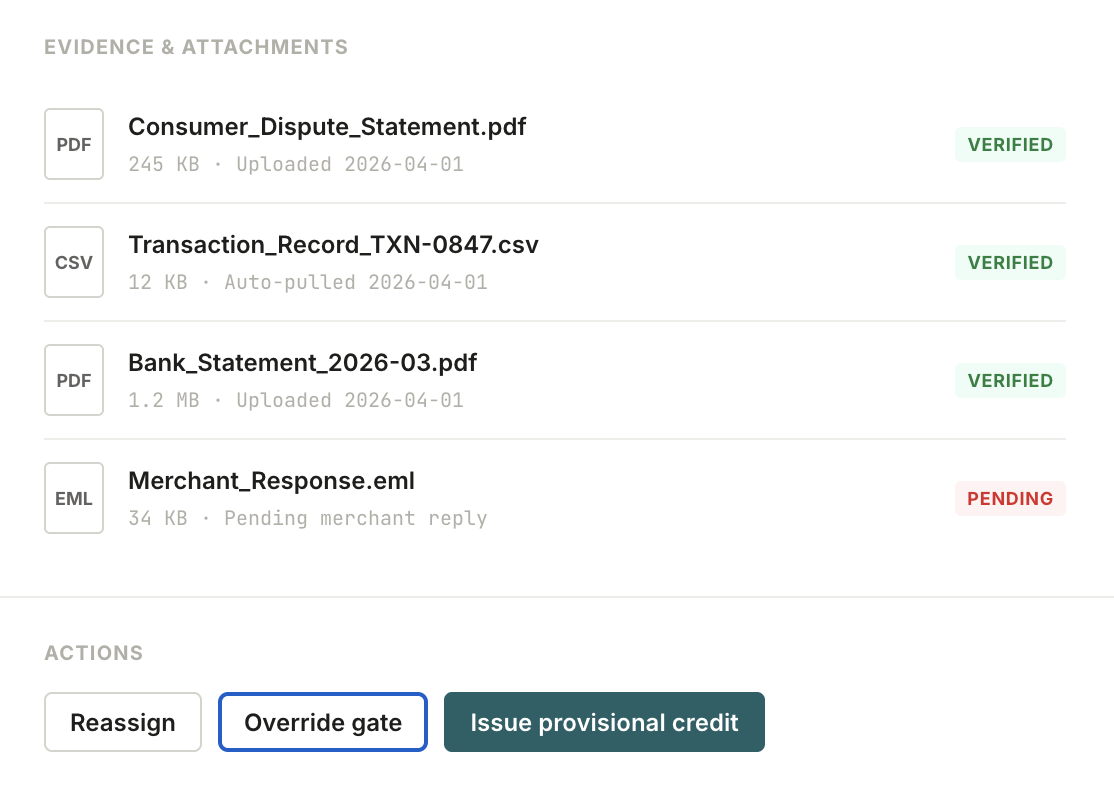

Every action, every gate passage, every escalation, and every human override is logged with timestamp, actor, and rationale. When the CFPB examiner asks "show me the timeline for Dispute #4721," your compliance team pulls a single document that answers every question. No reconstruction. No guesswork. The system was the audit trail from Day 0.

Every other tool in this market optimizes the workflow around compliance. DeadlineShield enforces compliance at the system level. The distinction matters when a CFPB examiner is reading your dispute logs.

| Capability | Fiserv / FIS | FINBOA | Quavo | DeadlineShield |

|---|---|---|---|---|

| Reg E deadline tracking | ✓ | ✓ | ✓ | ✓ |

| Reg Z billing error tracking | ✗ | ✓ | ✓ | ✓ |

| Card network dispute timelines (Visa, MC) | ✗ | ✗ | ✓ | ✓ |

| NACHA ACH return deadlines | ✗ | ✗ | ✗ | ✓ |

| Missed deadline blocks case advancement | ✗ | ✗ | ✗ | ✓ |

| Multiple concurrent clocks per dispute | ✗ | ✗ | ✗ | ✓ |

| Mandatory auditable override on blocked gates | ✗ | ✗ | ✗ | ✓ |

| Immutable append-only audit trail | ✗ | ✗ | ✗ | ✓ |

| Examiner-ready compliance reports | ✗ | ✓ | ✓ | ✓ |

| Institution-specific business day calendar | ✗ | ✗ | ✓ | ✓ |

| No core banking changes for pilot | ✗ | ✓ | ✗ | ✓ |

When the examiner arrives, they ask two questions: "Can you prove you met every deadline?" and "Can you prove your data is secure?" DeadlineShield is built to answer both.

AES-256 encryption for stored data. TLS 1.3 for all data in transit. No plaintext dispute data at any layer.

Granular permissions by role: analyst, compliance officer, examiner (read-only), administrator. No shared logins.

Every action timestamped with actor and rationale. No edits. No deletions. Append-only log that satisfies CFPB examination requirements.

Each institution's data is logically isolated. No cross-tenant access. Separate encryption keys per tenant.

Consumer financial data handled in accordance with Gramm-Leach-Bliley Act requirements for financial institution service providers.

Per-dispute timeline reports, compliance exposure summaries, and deadline adherence analytics exportable on demand. No manual assembly.

We are onboarding five banks or fintechs as design partners. You get the full DeadlineShield platform for 30 days while we calibrate the compliance enforcement engine against your institution's dispute workflow. In exchange, we co-author a case study and you introduce us to two peer institutions when the pilot completes.

DeadlineShield is a compliance enforcement engine that converts Reg E, Reg Z, and card network deadlines into gates that block a dispute from advancing until the required action is completed, with a full audit trail at every step.

For the design partner program, no core banking integration is required. DeadlineShield accepts dispute data via CSV upload or REST API. Your team continues to use their existing core banking system (FIS, Fiserv, Jack Henry) for transaction processing. Provisional credit posting remains a manual action in your core for the pilot. V1 builds API adapters for the Big Three core banking platforms so provisional credits can auto-post from a DeadlineShield gate trigger.

Yes. DeadlineShield enforces compliance clocks for Reg Z billing error disputes alongside Reg E EFT disputes. The same gate enforcement model applies: when a Reg Z acknowledgment deadline or resolution deadline arrives without the required action, the gate holds and escalates. It also covers Visa Claim Resolution and Mastercard chargeback timelines.

FINBOA is a workflow automation tool. It sends compliance alerts and routes disputes through configurable workflows. If a human misses an alert, the deadline passes and FINBOA logs it as overdue. DeadlineShield works differently: when a deadline arrives without the required action, the system holds the case and won't let you proceed until the action is taken. The failure mode in FINBOA is a missed email. The failure mode in DeadlineShield is a blocked gate that requires an explicit human override with an audit trail.

Quavo is the market leader in dispute workflow automation, with $300M in funding and 12.5M disputes per year. Quavo optimizes the dispute investigation workflow and recently launched ARIA, an AI investigation agent. DeadlineShield is focused on a different layer: compliance enforcement, not investigation automation. Quavo makes your investigators faster. DeadlineShield makes sure your institution never misses a deadline regardless of how fast your investigators are. In a mature deployment, Quavo and DeadlineShield could coexist: Quavo handles the investigation workflow, DeadlineShield enforces the compliance clocks.

ServiceNow offers dispute workflow with Visa integration and configurable routing. It is a strong workflow platform. DeadlineShield's enforcement gate model means missed deadlines are structurally blocked, not just flagged as overdue in a dashboard. ServiceNow tracks whether a deadline was met. DeadlineShield makes sure it is met by holding the case until the required action is completed.

Fiserv has two dispute products and neither enforces compliance at the gate level. Nautilus Efficiency Manager handles Reg E disputes with email-based deadline alerts. Dispute Expert handles credit card chargebacks with Ethoca integration. FIS CBK uses RPA for chargeback processing. All three are workflow and process tools. None of them block a case when a deadline is missed. They track compliance; they don't enforce it.

Your institution's holiday calendar (which days you close for business) and a sample of open dispute records with intake dates, dispute types, and current status. Data can be provided via CSV upload or programmatic API integration. Most compliance teams can export from their existing system in an afternoon. We handle normalization. No PII is required for the pilot setup phase; we work with synthetic data until you are comfortable with the platform.

A single consumer dispute can run four or more independent clocks simultaneously: the investigation deadline, the provisional credit deadline, the determination notification deadline, and the provisional credit reversal notice deadline. Each clock has its own gate. DeadlineShield tracks all of them independently, computes deadlines to the business day using your institution's calendar, and enforces each gate separately. This is the concurrent clock orchestration problem that spreadsheets and email alerts cannot solve.

DeadlineShield is built on the MightyBot agent platform. MightyBot is SOC 2 Type II certified and serves regulated industries including banking, lending, and insurance.

If DeadlineShield reduced your compliance exposure and your team trusts the enforcement gate model, we talk about a paid plan. If not, we shake hands and part ways. No auto-renewal, no lock-in, no surprise bill.

Five design partner slots. First come, first served. If your institution processes consumer disputes, the CFPB examination cycle is tightening and the penalties are getting larger. Make sure your compliance posture is structural, not aspirational.

Become a design partnerDispute data is sensitive consumer financial information. DeadlineShield runs on infrastructure built for institutions that answer to regulators.

MightyBot is SOC 2 Type II certified, following a successful audit by an independent firm. The certification confirms MightyBot meets the rigorous standards of Security, Confidentiality, and Availability required to process sensitive consumer dispute data, investigation records, and compliance audit trails. Every data access is logged; every agent action is auditable end to end.